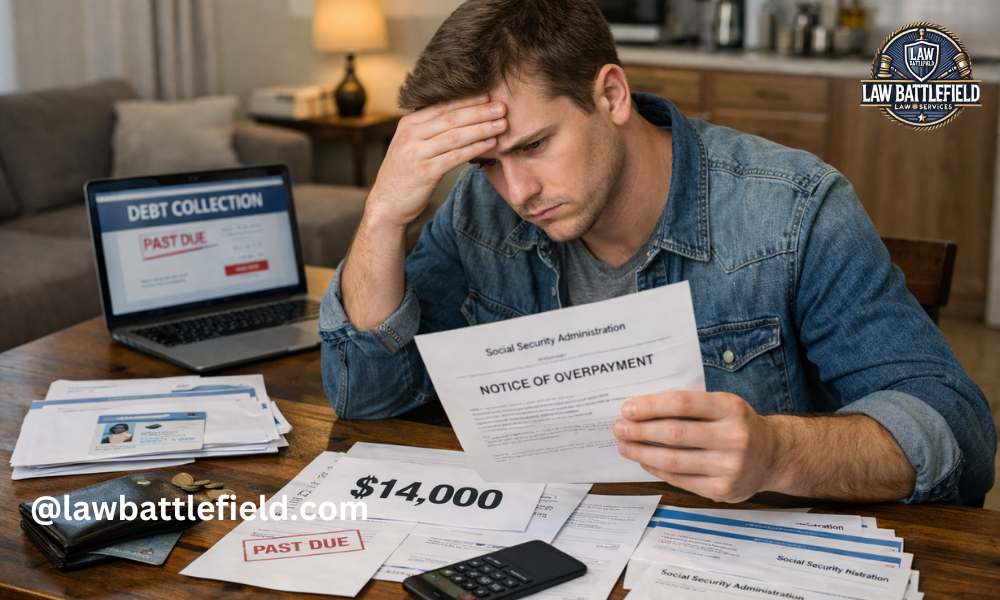

If a young adult has a $14,000 Social Security overpayment debt, it can feel confusing and overwhelming at first. Many people in this situation are surprised, especially if the benefits were received years ago during childhood. In simple terms, a Social Security overpayment happens when the government believes it paid more money than it should have.

This issue often affects young adults because benefits like survivor or disability payments are sometimes managed by parents or guardians. In other cases, errors in records, delayed updates, or even identity theft can lead to unexpected debt notices later in life.

The good news is that you are not powerless. There are clear rules, legal rights, and practical steps you can take to understand the situation, challenge it if needed, or manage repayment in a way that works for you. This guide will walk you through everything in plain, easy-to-understand language.

Handling a $14,000 SSA Overpayment

| Aspect | Details |

| What It Means | SSA believes you were paid more benefits than allowed |

| Common Cause | Childhood benefits, reporting delays, SSA errors, identity theft |

| Who Is Affected | Often young adults whose benefits were managed by guardians |

| First Step | Request official Notice of Overpayment from SSA |

| Check Carefully | Dates, amounts, reasons, eligibility history |

| Main Options | Appeal (Reconsideration) or Request Waiver |

| Key Deadline (30 Days) | Stops collection if you respond quickly |

| Final Deadline (60 Days) | Time limit to file appeal |

| Waiver Eligibility | Not your fault + cannot afford repayment |

| Repayment Option | Flexible monthly plans (as low as small amounts) |

| Benefit Withholding | Usually limited to ~10% of monthly benefits |

| Identity Theft Action | Check credit report + report fraud immediately |

| Help Available | Legal aid, SSA offices, congressional caseworkers |

| Important Tip | Never ignore notices—early action protects you |

Understanding Social Security Overpayment in Young Adults

A Social Security overpayment simply means that the Social Security Administration (SSA) believes you received more money than you were eligible for. This can happen for many reasons, and it does not always mean someone did something wrong.

The SSA tracks benefits based on eligibility rules such as income, disability status, or family circumstances. If those conditions change and are not updated in time, the system may continue sending payments that later get flagged as overpayments.

Young adults are often affected because the benefits were originally issued when they were minors. At that time, a parent or guardian usually handled the payments. Years later, when the SSA reviews records or updates information, the responsibility may shift to the individual, even if they had no control over the situation.

Common Reasons Behind a $14,000 Overpayment Debt

When a young adult has a $14,000 Social Security overpayment debt, it is usually linked to specific situations rather than random errors.

One common reason is benefits received during childhood, such as survivor benefits after the loss of a parent or disability benefits. These payments are often managed by an adult on behalf of the child, and mistakes in reporting or eligibility can lead to overpayments.

Another reason is changes in eligibility that were not reported on time. For example, if a household’s income changed or a disability status was updated, but the SSA was not informed quickly, payments may have continued incorrectly.

Sometimes, the issue comes from administrative errors. This could be a mistake made by the SSA or incorrect information provided by a guardian. In these cases, the young adult may not have been aware of the problem at all.

Identity theft is another possible cause. If someone used your Social Security number without permission, benefits may have been issued in your name, leading to debt that you never actually received.

How to Confirm If the Debt Is Accurate

Before taking any action, it is important to confirm whether the debt is correct. The first step is to request an official Notice of Overpayment from the SSA. This document should clearly explain why the overpayment happened, the time period involved, and how the amount was calculated.

Carefully review all the details in the notice. Look at the dates, the total amount, and the explanation provided. Even small errors in these details can change the outcome.

It is also helpful to review personal and family records. If the benefits were received during childhood, speak with your parents or guardians to understand what happened at that time. They may have information that explains the situation or reveals an error.

If anything does not seem right, do not ignore it. Questioning the details early can make a big difference in how the case is handled.

Your Legal Rights When Facing an Overpayment

If a young adult has a $14,000 Social Security overpayment debt, it is important to know that there are legal protections in place.

You have the right to receive a clear explanation from the SSA about why the overpayment occurred. The agency must provide enough detail for you to understand the situation.

You also have the right to challenge the decision. If you believe the amount is wrong or that you were never overpaid, you can file an appeal, also known as a reconsideration.

In addition, you have the right to request a waiver. This applies if the overpayment was not your fault and you cannot afford to pay it back. Many young adults qualify for this, especially if the issue relates to benefits received during childhood.

There are also protections related to collections. In certain cases, if you act quickly, the SSA must pause collection efforts while your case is being reviewed.

Steps to Take Immediately After Discovering the Debt

The moment you find out about the debt, taking the right steps can help you stay in control of the situation.

Start by contacting the SSA and asking for all related documents. This ensures you are working with complete and accurate information. If you only saw the debt online, getting the official notice is especially important.

Next, consider the possibility of identity theft. If you do not recognize the benefits or payments, check your credit history and look for any unusual activity.

If the benefits were received during childhood, talk to your parents or guardians. They may be able to explain how the benefits were used and whether any issues were known at the time.

Finally, organize all your documents. Keeping everything in one place will make it easier to respond, file forms, or seek help if needed.

Step-by-Step Quick Action Guide

- Get the official SSA notice (don’t rely only on online info)

- Review all details carefully (dates, amounts, reasons)

- Talk to parents/guardians if benefits were from childhood

- Check for identity theft if something feels wrong

- Decide your path → appeal (if incorrect) or waiver (if not your fault)

- Act within 30 days to stop collections

- Seek help if needed (legal aid or SSA support)

How to Dispute the Overpayment (Reconsideration Process)

Disputing the overpayment is the right step if you believe the debt is incorrect. This process is called reconsideration.

You should consider this option if the amount seems wrong, if you never received the benefits, or if there is missing or incorrect information in the notice. Filing for reconsideration allows the SSA to review your case again.

There are important deadlines to keep in mind. Acting quickly is important because it can affect whether collections are paused during the review process.

After you submit your appeal, the SSA will examine the evidence and make a decision. This may take some time, but it gives you a chance to correct errors and avoid paying a debt that is not valid.

When and How to Request a Waiver

A waiver is different from an appeal. Instead of arguing that the debt is wrong, you are asking the SSA to forgive it.

This option is available when the overpayment was not your fault and repaying it would cause financial hardship. Many young adults qualify for waivers, especially if they had no role in managing the benefits.

To request a waiver, you will need to explain your situation clearly. This includes showing that you did not cause the overpayment and that paying it back would be difficult.

The SSA will review your financial situation and the details of the case before making a decision. In many cases, waivers are granted when the circumstances are reasonable.

Understanding the 30-Day and 60-Day Deadlines

Timing plays a major role when dealing with a Social Security overpayment.

If you respond within 30 days of receiving the notice, the SSA is generally required to pause collection efforts. This can provide relief while your case is being reviewed.

There is also a 60-day deadline to file an appeal. Missing this window can make it harder to challenge the debt, although there may still be options in some situations.

Acting early gives you more control and protects you from unnecessary stress or financial pressure.

Flexible Repayment Options If You Owe the Debt

If it turns out that the debt is valid, you still have options. The SSA understands that paying a large amount like $14,000 all at once is not realistic for most people.

You can request a monthly payment plan based on what you can afford. In some cases, payments can be as low as a small amount per month.

If you are currently receiving Social Security benefits, the SSA may withhold a portion of those payments. However, current policies limit how much can be taken, helping to prevent financial hardship.

The key is to choose a repayment plan that fits your situation. Open communication with the SSA can make this process smoother.

How Identity Theft Can Lead to Social Security Debt

Identity theft is a serious issue that can sometimes lead to unexpected Social Security debt.

If someone used your Social Security number without permission, benefits may have been issued in your name. This can result in an overpayment notice even though you never received the money.

Signs of identity theft include unfamiliar activity on your credit report or benefits you do not recognize. If you suspect this, it is important to act quickly.

Reporting the issue and providing evidence can help resolve the case and remove responsibility for the debt. It may also involve additional steps to protect your identity in the future.

Getting Professional Help and Support

Dealing with a Social Security overpayment can feel complicated, but you do not have to handle it alone.

Legal aid services are available for individuals with limited income. These organizations can help you understand your rights and guide you through the process.

In more complex cases, professional advice can make a difference. Experts can help you prepare documents, meet deadlines, and present your case clearly.

You can also contact your congressional representatives. Their offices often have staff who assist with issues involving federal agencies, including the SSA.

Mistakes to Avoid When Dealing With SSA Overpayment

Many people make simple mistakes that can make the situation harder than it needs to be.

Ignoring notices or missing deadlines can lead to faster collection actions. It is always better to respond, even if you are unsure what to do next.

Another common mistake is assuming the debt is correct without checking. Errors do happen, and reviewing the details is essential.

Missing documents can also weaken your case. Keeping records organized helps you respond more effectively.

Finally, not exploring all available options can limit your chances of resolving the issue. Whether it is an appeal, waiver, or repayment plan, understanding your choices is key.

Conclusion

If a young adult has a $14,000 Social Security overpayment debt, it may seem overwhelming at first, but there are clear paths forward. Understanding the reason behind the debt is the first step, followed by reviewing your rights and taking timely action.

In many cases, solutions such as appeals, waivers, or flexible repayment plans can reduce or even eliminate the burden. The most important thing is not to ignore the situation. Acting early, asking questions, and seeking help when needed can make a significant difference.

With the right approach, this challenge can be managed, and you can move forward with greater confidence and peace of mind.

FAQs

Why Does A Young Adult Have A $14,000 Social Security Overpayment Debt?

This usually happens due to benefits received during childhood, reporting delays, SSA errors, or identity theft involving your Social Security number.

Can I Avoid Paying A Social Security Overpayment?

Yes, if the overpayment was not your fault and you cannot afford repayment, you can request a waiver to have the debt reduced or completely removed.

What Happens If I Ignore The SSA Overpayment Notice?

Ignoring it can lead to collections, including tax refund offsets or benefit reductions. It’s always better to respond and explore your options early.

How Long Do I Have To Appeal A Social Security Overpayment?

You generally have 60 days to appeal, but filing within 30 days can stop collection actions while your case is reviewed.

Can I Pay The $14,000 In Small Monthly Payments?

Yes, the SSA allows flexible repayment plans based on your financial situation, sometimes with very low

monthly amounts.

Was this article helpful? Check out more on Lawbattlefield.com

Disclaimer: This article is for informational purposes only and does not provide legal or financial advice. Policies and rules may change over time. For personalized guidance, please contact the Social Security Administration or a qualified professional.